The concept of investing broadly covers the purchase or creation of assets with the use of funds or capital in order to obtain a return on the investment, also known as capital gain. It entails the purchase of a financial product with an expectation of favourable future returns. Investment assets comprising equities, fixed income instruments, derivative instruments, commodities, etc., are purchased with the sole aim of earning the maximum possible return.

Over the years, researchers have developed various approaches and models for driving optimal returns on various investment products. The two major approaches to investing include Factor Investing and Value Investing. These models were developed to ensure optimal asset allocation and maximum return on investment. This article seeks to analyze the fundamentals of the Factor approach to investing, the various types of Factor Investing and its numerous benefits.

Understanding Value Investing

Value investing is an investment approach that seeks to leverage the value of underpriced or cheap stocks on the expectation that improving market conditions and strong corporate fundamentals will be priced into the value over time. The strategic asset allocation expectation is that the stock price will rise as its intrinsic value becomes more evident and widely acknowledged by investors. When the stock price rises to its intrinsic value over a given time frame, this translates to an increase in the value of the investment portfolio through capital gains and dividend cashflow. The greater the difference between the intrinsic value and the current stock price, the greater the margin of safety for value investors looking for investment opportunities.

Key financial metrics (such as earnings, revenue, or cash flow) are usually deployed to determine the value of a stock. Other characteristics considered during the stock valuation process include consistent profitability, stable revenue streams with reasonable growth, future earnings outlook and a long streak of established success history.

Understanding Factor Investing

Factor Investing is an Investment approach that involves targeting specific drivers of a return across asset classes with the goal of achieving a given investment outcome or improving long-term risk-adjusted return. The drivers of return are called “Factors”, and they form the foundations of factor investing. At its most basic level, factor-based investing is simply about defining and then systematically following a set of rules that produce diversified portfolios. The underlying assumption is that an investor can build a portfolio that consistently outperforms the market by examining assets under defined characteristics.

The Role of Factors as Drivers of Risk and Return

- The Capital Asset Pricing Model (CAPM) advancement has shown great potential for factor-based strategies to play a key role in diversified portfolios. The identification of the CAPM “beta” (the measure of the sensitivity of a stock to the movement of the broader market) and other factors/betas that drive risk and return has established the importance of factor investing.

- Factor analysis also helps explain the behaviour of portfolios in ways that were previously not understood using historical patterns/behaviour of the portfolios.

The concept of factor investing would prove useful for fund managers in active portfolio management, corporate treasurers as part of liquidity management and individual investors. Investment decisions at all levels seek to determine the preferred asset allocation mix that satisfies risk and return constraints. With the aid of factor investing, investors seeking to maximize the return on their investment at a given level of risk exposure can achieve their objective.

Understanding the types of factors and their importance

Generally, two main factors drive portfolio returns: Macro Factors explain broad risks across asset classes like the pace of economic growth and inflation rate, which in turn provides an explanation for the returns on asset classes. On the other hand, Style Factors explain the risk and returns within these asset classes. For instance, low priced stocks are more likely to generate higher returns than high priced stocks.

A. Style Factors

- Size – Research has proven that smaller-cap stocks yield a higher return premium. This is sometimes attributed to the inherent risky nature of these stocks. Smaller companies are typically more volatile and are exposed to a higher risk of bankruptcy. As such, investors seek to be compensated for taking on the additional level of risk.

- Value – This is the second factor introduced in the Fama-French model. It suggests that inexpensive stocks should outperform expensive stocks. According to Graham (1949), the belief is that expensive stocks with lofty expectations leave room for error, while cheaper stocks that can beat expectations may afford investors more upside.

- Momentum – This entails examining price trends to forecast future returns. Empirical evidence, first published in 1993 by Narasimhan Jagadeesh and Sheridan, demonstrated that stocks that had outperformed in the medium term would continue to perform well, and vice-versa for stocks that had lagged.

- Quality – This style of investing is based on company performance and selection is based on financially healthy company stocks or debt securities. The position is that companies that generate superior profit, possess strong balance sheets, and strong cash flows can provide optimal return and outpace the market over the long term.

- Low/Minimum Volatility – Owning stocks with lower risk or return volatility than the broader market has historically resulted in higher risk-adjusted returns. Research has also shown that low-volatility portfolios have the potential to outperform the broader market over time.

B. Macroeconomic Factors

Key macroeconomic factors are outlined below;

- Economic Growth – Fluctuations in the business cycle is a key factor in investing as various asset class returns are affected by changing economic activities and business cycles. Some economic sectors perform well in recession, recovery and growth phases while some sectors are adversely affected in recessions and only do well in growth phases of the economy. A careful consideration of the performance of companies operating in different economic sectors, and their asset price performance in different phases of the business cycle will provide empirical data for factor investment selection.

- Interest Rates – The direction of interest rate movements determines the selection of an asset class; equity, commodities, derivatives, real estate, or fixed income investments to be considered given the correlation of interest rates, fixed income yield, real estate prices, commodity prices, derivative value and stock prices.

Nigeria Policy rate versus 10Yr FGN Bond Yield

The graph above shows the relationship between Nigeria’s policy rate and 10year FGN bonds yield over the last 10years. The trend shows some correlation, thus the direction of interest rate will be a good factor for bond investing.

Nigeria Policy rate versus Stock Market Index

The chart above plots the relationship between Nigeria’s policy interest rate and the stock market index over a 10year period. A close look at the graph shows a low correlation between the two factors and it can be deduced that other micro and macro factors beyond the movement of the policy interest rate were driving stock index prices.

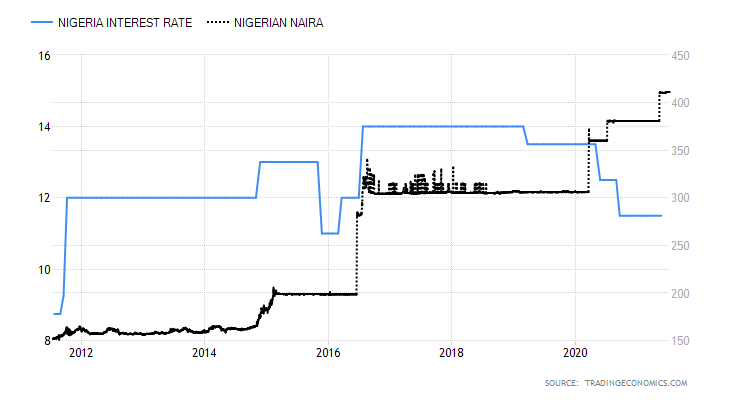

Nigeria Policy rate versus Naira Exchange Rate

- Inflation: The general rise in prices of goods and services impact the value, cash flow and return of various asset classes depending on the cause of inflation. If inflation is due to an increase in money supply, it could lead to financial assets price inflation (or bubble) and this is considered in asset selection and factor investing.

- Credit: Default risk from borrowing companies may be aggravated in a recession and minimal in a recovery or growth phase of the economic cycle. Asset managers consider this in allocating portfolios to companies and sectors their credit risk and the impact of the economic cycle on their performance. Sectors that thrive in a recession tend to receive the highest credit allocation during recessions while other sectors adversely impacted by a recession receive the lowest allocation. By so doing, active asset managers balance their investment and generate improved risk-adjusted returns through a given business cycle.

- Emerging Markets – Political and sovereign risks: Political and sovereign risk factors are key elements in factor investing as a weak or unstable polity, sovereign downgrades or defaults can adversely affect economic sectors and asset classes in the affected country and harm investment returns. Diversification across industry sectors and across countries may not ameliorate political and sovereign risk factors.

- Liquidity: Liquidity of the market and liquidity of the asset class plays a critical role in asset selection as the value, return/price volatility and saleability of assets are influenced by this factor.

Background to the development of Factor Investing

The foundation of factor investing begins with the Capital Asset Pricing Model, a mathematical expression that tries to quantify the drivers of an individual asset or portfolio returns while accounting for risk exposures. This is also known as the “One Factor” model as it accounts only for market risk. This was expanded further by Eugene Fama and Kenneth French when they accounted for size risk and value risk (Fama & French, 1992). The expanded CAPM model was able to explain asset or portfolio outperformance with a greater level of accuracy. This was also known as the three-factor model. Overall, the model was able to explain about 90% of the difference in asset returns.

Mark Carhart built on the Fama three-factor model by adjusting for momentum in explaining asset returns. In his paper “On Persistence in Mutual Fund Performance,” (Carhart, 1997), he defined the momentum factor as the average return of the top 30% of stocks minus the average return of the bottom 30% as ranked by this measure. According to Berkin & Swedroe (2016), the addition of momentum to the three-factor model increased the explanatory power of the model by 5%Expanding on Mark Carhart’s model, Robert Novy-Marx and Alan S. Zekelman added the quality or profitability factor to the model. Quality or profitability factor adopted by Benjamin Graham defines low quality in an enterprise as low debt, long history of paying dividends and earnings growth.

Applying factor Investing in Fixed Income

Despite the importance of factors, factor-based investing in fixed income has been slow to develop and remains a developing area of study. This is driven partly by the lack of data, relatively opaque pricing, and a relative lack of transparency in the asset class. Another challenge identified in applying factor investing to Fixed Income assets is that the various segments of fixed income markets make it difficult to create a one-size fits all factor investing model. However, factors may be even more critical in fixed income, as systematic risk constitutes a significant proportion of bond total risk.

Fixed income markets are, by nature, more reliant on systematic drivers than equity markets and the outperformance of a significant portion of fixed income portfolios have been driven by exposure to systemic risk (Khan, 2015). Soe & Xie (2016) identified that the combination of uncorrelated or low-correlated fixed income risk factors potentially allows for smooth return patterns and may offer portfolio diversification benefits over market cycles. All things being equal, the more volatile the bond yield is, the higher the yield needs to be in order to compensate for the volatility risk. Higher exposure to the value factor may be used to seek enhanced returns, while lower exposure to the low-volatility factor may be used to mitigate risk.

In assessing government and corporate bond indices, the usual weighting of securities based on market capitalization poses a peculiar challenge because it implies that high weightings are assigned to the most highly indebted countries and companies, respectively. Investors will therefore be disproportionately invested in issuers with the highest debt burden. In addition, debt indices are often less balanced than equity indices.

While there exists an extensive body of literature evaluating the use of factor-based models in developed markets, we have limited insight into its application in emerging markets like Nigeria. The following constraints have been identified for implementing factor investing in the Nigerian capital markets (Fixed Income and Equities)

- Limited data availability for backtesting

- Lack of market depth and efficient price discovery

- Lack of liquidity in the corporate debt market.

As the market develops, the expectation is that investors would have access to larger data sets and the diversity of the asset pool would increase. This would see to increased efficiency in decision making as well as a data-driven approach to generating alpha returns.

References

- Acuity Knowledge Partners. (2019). Whitepaper – Factor-Based Investing. Ney York: Acuity Knowledge Partners.

- Berkin, A. L., & Swedroe, L. E. (2016). Your Complete Guide to Factor-Based Investing. St Louis: Bam Alliance Press.

- Carhart, M. M. (1997). On Persistence in Mutual Fund Performance. The Journal of Finance, 57-82.

- Fama, E. F., & French, K. R. (1992). Common Risk Factors in the Returns of Stocks and Bonds. Journal of Financial Economics, 1-56.

- Hoepner, A., & Ditfurth, M. (2017). Whitepaper: Sustainable Factor Investing. New York: Invesco.

- Khan, R. a. (2015). Smart Beta: The Owner’s Manuel. The Journal of Portfolio Management, 41(2), 1-10.

- Soe, A. M., & Xie, H. (2016). Factor-Based Investing in Fixed Income: A Case Study of the U.S. Investment-Grade Corporate Bond Market. New York: S&P Global.

- Dan Caplinger (2021). The Value Investing Strategy. TMFGalan.

- Darby, N., Frank N., & Bobby, B. (2015). An Overview of Factor Investing. Fidelity Investments.

- BlackRock., https://www.blackrock.com/us/individual/investment-ideas/what-is-factor-investing

- Blaise, W., & Stephen., Q. (2019). Foundational Concepts for Understanding Factor Investing. Invesco