The monetary policy committee (MPC) meets today and tomorrow. At its last meeting held in May, the committee was faced with two broad options: address the high inflationary pressure or pursue measures to support the economic recovery. See more details below.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) weakened by 0.27% to close at N411.50/US$1. On the other hand, in the parallel (or street) market, the naira appreciated by 0.40% to close at N504.00/US$1. Currently, the gap between the I&E window and the parallel market stands at 22.48%. Last week, the CBN’s reported FX reserves rose by 0.23% to US$33.17bn. At levels of liquidity in the I&E Window and NAFEX markets well below what they were early last year (before the divergence between the NAFEX and parallel rates), we expect the parallel and the I&E Window rates to remain under pressure over the months to come.

Bonds & T-bills

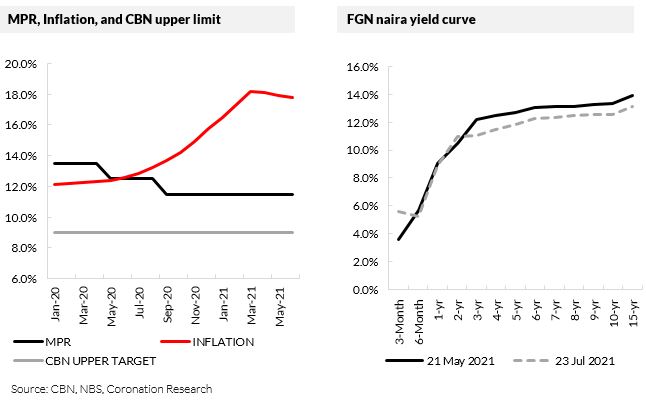

Last week, trading in the secondary market for FGN bonds was bullish as investors reacted to the fall in stop rates at the primary auction. The yield of an FGN Naira-denominated bond with 10-years to maturity was down by 9bps to 12.56%, the yield on the 7-year bond was down by 2bps to 12.33%, and the yield on the 3-year bond also fell by 2bps to 11.08%. The overall average benchmark yield fell by 7bps w/w to close at 12.09%. At the bond primary auction, the Debt Management Office (DMO) offered N150.00bn across three tenors. The DMO eventually allotted N241.97bn worth of bonds (N138.07bn from competitive bids and N103.90bn from non-competitive bids). Stop rates eased on average for the second successive auction, with the rates on the FEB-2028 (-39bps to 12.35%), MAR-2036 (-35bps to 13.15%), and MAR-2050 (-45bps to 13.25%) bonds all declining. Although the auction was oversubscribed, demand was not as strong as the previous auction (bid-to offer: 1.91x vs 2.78x previously).

Similarly, activities in the Treasury Bill (T-bill) secondary market was bullish, on the back of liquidity-driven demand in the OMO segment at the start of the week. The annualised yield on a 356-day T-bill in the secondary market closed at 8.87%, while the yield on a 235-day OMO bill fell by 129bps to 9.03%. While the average benchmark yield for T-bills rose by 20bps w/w to close at 6.90%, the average yield for OMO bills fell by 73bps w/w to close at 8.57%. Selloffs were concentrated at the short end of the T-bill curve, while demand was strong across the entire OMO curve as investors reinvested the last of the previous week’s bond inflows. At this week’s T-bill PMA, the DMO is expected to offer N216.19bn worth of bills across all tenors.

Oil

Last week, the price of Brent crude recorded its first weekly gain (+0.69% w/w) since the beginning of the month, closing at US$74.10/bbl and showing a 43.05% increase year-to-date. The average price year-to-date is US$66.30/bbl, 53.41% higher than the average of US$43.22/bbl in 2020. Oil prices plunged 7% on Monday on worries about the increased OPEC+ supply and the spread of the delta variant of the coronavirus and its impact on energy demand. However, oil prices rebounded as investors felt supply will still struggle to keep up with recovering global demand, and as a result, were eager to buy the dip. We reiterate our view that the price of Brent oil is likely to remain well above the US$60.00/bbl mark for several months.

Equities

The NGX All-Share Index (NGX-ASI) was up by 1.90% last week. Consequently, the year-to-date return rose to -3.98%. Oando +20.67%, Unilever Nigeria +9.58%, and Guinness Nigeria +9.14% closed positive while International Breweries -2.80%, Sterling Bank -2.56%, and Stanbic IBTC -0.73% closed negative last week. Sectoral performances were broadly bullish, with the NGX Oil and Gas +7.53%, NGX Industrial index +4.06%, NGX 30 +1.94%, NGX Consumer Goods +0.57%, and the NGX Banking index +0.44% all closing the week positive. The NGX Insurance index was the sole loser, declining by 0.74%. The Model Equity Portfolio will resume next week. The Model Equity Portfolio will resume next week.

The monetary policy committee (MPC) meets today and tomorrow. At its last meeting held in May, the committee was faced with two broad options: address the high inflationary pressure or pursue measures to support the economic recovery.

One factor considered at the meeting in May was the economy’s exit from recession by Q4 2020. However, GDP growth remains fragile at 0.51% recorded in Q1 2021. Meanwhile, headline inflation had witnessed a marginal decline in April to 18.12% y/y from 18.17% recorded in the previous month. The MPC had stated that inflation was primarily a result of a combination of factors, such as the heightened security tensions in the country and deteriorating public infrastructure rather than the monetary policy rate, and decided to hold all policy parameters constant.

We expect the GDP figures for Q2 to be positive, given base effects and improved economic activity. The spread of the Delta variant of the coronavirus is likely to give the committee some concern around the global and domestic economic outlook. However, the resilience of the vaccines should help maintain a strong outlook for recovery. Although the argument for tackling inflation is compelling, we note that headline inflation declined for the third consecutive month from 17.93% y/y in May to 17.95% y/y in June (however, it is still well above the CBN’s target range of 6% – 9%). This downward trend was driven by a marginal slowdown in food inflation to 21.83% y/y in June from 22.28% y/y recorded in May. We note that imported food inflation rose to 17.22% y/y in June 2021 from the 16.97% y/y recorded in the previous month.

Since May, bond yields have also declined marginally on the back of strong demand for FGN debt instruments, while the equity market, though stable, is down -3.98% year to date. Exchange rate pressures resulting from capital flow reversals have not improved, and exchange rate speculations have continued to fuel the depreciation of the naira in the parallel market to N504/US$1 as of 23 July 2021. Although oil prices have improved (Brent crude closed at US$74.1/bbl on Friday), external reserves have continued to decline from US$34.29bn in May to US$33.17bn as of 19 July. Given the committee’s view that output growth will continue to recover for the rest of 2021 as well as inflation on a downward trend, the committee is likely to maintain its current strategies, such as:

- the continuous use of cash reserve ratio (CRR) debits to mop up liquidity in the banking industry,

- the use of its intervention facilities such as the Anchor Borrower Program, Targeted Credit Facility and Agri-Business Small and Medium Enterprise Investment Scheme (AGSMEIS).

Our view is that the committee will make no changes to its current stance.

Nota bene: The Coronation Research Model Equity Portfolio is an expression of opinion about Nigerian equities and does not represent an actual portfolio of stocks (though market liquidity is respected and notional commissions are paid). It does not constitute advice to buy or sell securities. Its contents are confidential to Coronation Research up until publication. This note should be read as an integral part of the disclaimer that appears at the end of this publication.