The Monetary Policy Council (MPC) of the Central Bank of Nigeria (CBN) meets this week to consider its policy rate and the overall direction of interest rates. As we pointed out last week, the upward movement in the CBN’s foreign exchange reserves, combined with the positive direction in oil prices and the stock market, gives the MPC room for manoeuvre. And with Q1 2020 GDP today reported as growing 1.87% y/y, we believe a pro-growth stance will be maintained; no change in the 13.50% policy rate and little (if any) pressure to raise market interest rates. Read more below…

FX

Month-to-date the FX reserves of the CBN are up US$1.87bn to US$35.77bn. Inflows are now largely from the public sector, in our view, notably supra-national lending to the Federal Government. By contrast, the combined month-to-date inflow from foreign direct investment (FDI) and foreign portfolio investment (FPI) is just US$40.1m (N15.6bn). Significant inflows from the private sector (such as the US$1.7bn received in January, for example) are unlikely to resume until oil prices trend above US$50.00/bbl, in our view. And we believe that oil prices above US$50.00/bbl are some way off. In the interbank market Naira is quoted at N390.57/US$1: in the parallel market US dollars are bid at N455.00/US$1.

Bonds & T-bills

The secondary market yield for a Federal Government of Nigeria (FGN) Naira bond with 10 years to maturity declined last week by 6bps to 11.19%, and at 3 years fell by 8bps to 9.09%. The annualised yield on 265-day T-bill, remained flat at 3.07%, while a CBN Open Market Operation (OMO) bill with similar tenure closed at 6.49%, 466bps down week-on-week. Last week activity in the T-bill market was bullish, spurred by demand as local investors were caught between managing liquidity and yield in their portfolios. The market is very liquid and the Debt Management Office (DMO) has no problem in over-allocating its auctions. We still think that overall pressure on market rates is upwards but, given significant system liquidity, only gently so.

Oil

The price of Brent crude rose by 8.09% last week to US$35.13/bbl. The average price, year-to-date, is US$42.73/bbl, 33.44% lower than the average of US$64.20/bbl in 2019, and 40.40% lower than the average of US$71.69/bbl in 2018. Oil prices have rallied since the start of new OPEC+ cuts on 1 May 2020. These cuts, along with improved global oil demand, have supported the price increases, but the bullish sentiment raises some questions. For example, will producers be tempted by rising crude oil prices to disregard quotas within OPEC? Will U.S. shale producers resume drilling activity sooner than the market needs it? The rally is undeniable but the key question of how far it will go is difficult to answer. OPEC and Russia seem not to want a return to the levels above US$50.00/bbl seen at the start of the year.

Equities

The Nigerian Stock Exchange All-Share Index (NSE-ASI) gained 5.59% last week. The year-to-date return is negative 6.10%. Last week Unilever Nigeria (+33.86%), Mobil (+20.92%), Okomu Palm Oil (+16.98%), PZ Cussons (+14.44%) and Zenith Bank (+9.71%) closed positive, while Nestle Nigeria (-4.33%) was the only stock on Coronation-30 list that closed negative. Performance across all sectors was positive. The Industrial Goods (+15.5%) index led the return chart, followed by the Banking (+7.2%), Oil and Gas (+4.9%), Insurance (+2.0%), and Consumer Goods (+0.9%) indices. The market is in full spate, suggesting a period of short-term profit-taking is coming up. On the other hand, we may soon have to revise our market call: this looks like a recovery in earnest. See Model Portfolio on page 3 for our assessment.

The long-term interest rate question

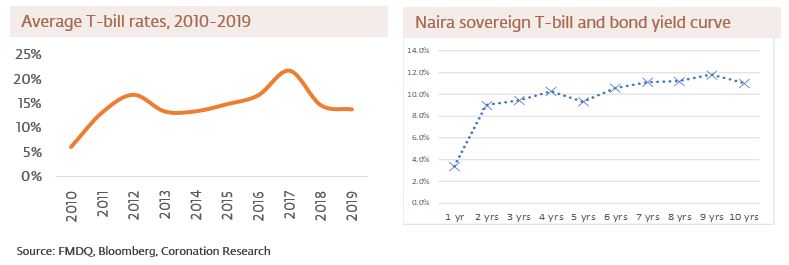

Which way are interest rates going to move? The question is relevant this week as the Monetary Policy Committee (MPC) of the Central Bank of Nigeria (CBN) meets. While most people think that the MPC will maintain its policy rate of 13.50% (a rate it seldom changes), the real question is what it wants to do with market interest rates. The 1-year T-bill rate is 3.07% compared with inflation which registered 12.34% year-on-year in March. This arrangement of rates and inflation is sometimes known as a subsidy for economic growth.

The bond market looks at low T-bill rates with nervousness. It allocates much higher yields to Naira bonds with a duration of 3-years than 1-year T-bills. The implication is that investors believe market interest rates will rise. Indeed the long-term lesson (over 10 years) of Naira T-bill rates is that they move up when the currency is under stress (2017 was a perfect example) as the authorities re-establish its attractiveness to foreign investors.

Is the long-term lesson of Naira interest rates relevant right now? As we wrote last week, the foreign exchange reserves of the CBN have been trending up recently (reversing a nine-month decline) and stand at US$35.8bn, a healthy level when viewed from a historical perspective. And the CBN also showed, ahead of the meeting of the MPC in March, that economic growth is its priority, a resolve that might be strengthened by today’s report of Q1 2020 GDP growth at a sluggish 1.87% year-on-year.

In fact, we doubt that the CBN is going to abandon its pro-growth stance this week. And, in order to do this, it will have to tough-out two difficult factors. The first is inflation, which is well above its target range of between 6.0% and 9.0%. The second is that turnover on the most-used foreign exchange market, the NAFEX market (also known as the Importers and Exporters Window), which supplies the interbank exchange rate given on Bloomberg, fell to a trickle in mid-March and remains below historical averages. The CBN may consider other ways of encouraging foreign exchange flow to pick up, in our view.

Implications for Naira fixed-income investors

How about investors? Over the past 10 years, 2010-2019 inclusive, Naira-based investors in T-bills have had a great time. They have received, on average, a risk-free spread of 2.57% over the rate of inflation. This has been good news for the 8.6 million holders of Naira-denominated retirement savings accounts (RSA). Sums held in money market funds have risen rapidly over the past three years. But, clearly, there is no risk-free spread over inflation to be had today (not even in bonds).

What happens if the CBN continues to hold market interest rates down? Investors will have to be more creative than in the past. Rather than holding just portfolios of T-bills they will have to diversify into other fixed-income instruments: commercial paper, promissory notes, state bonds, corporate bonds, bank deposits, and other instruments. Most of these involve a degree of risk, so risk management will emerge as the key skill.

And the direction of market interest rates? Our view is that there will be gentle upwards pressure on rates as the Debt Management Office (DMO) of the Federal Government goes about financing the deficit. But this does not necessarily mean a return of risk-free rates to the generous levels we have seen in the past. The market may have to wait a long time for that.

Model Equity Portfolio

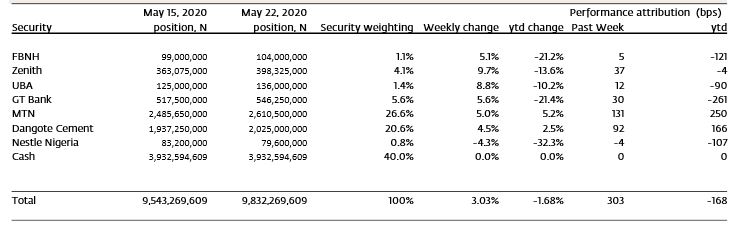

Last week was a bad week for the Model Equity Portfolio. It rose by 303 basis points (bps) but the index rose by 559bps. What went wrong? The obvious point is that we are holding far too much notional cash and that we are under-invested in equities. But there is more to it than that.

Our investment approach is to buy stocks with strong (generally above 21% per annum) return on equity (RoE) and reasonable growth prospects and to buy them when their valuations are low. We like the principal banks, and MTN Nigeria and Dangote Cement. Two weeks ago we quoted Oaktree’s Howard Marks to the effect that, while it is impossible to catch the bottom of the market, it is prudent to buy stocks you believe in when valuations are low. And then we increased our notional position in MTN Nigeria. So far, so good.

But what of our bank positions? We missed the blindingly obvious fact that we only have neutral positions in these which would not deliver enough upside if we did not increase them. We wrote that we would “re-calibrate these notional positions against their weights in the index” and then did not perform the task. Two big mistakes.

Of course, when we were out-performing the market by 848bps at the beginning of April, we could have taken the opportunity to build a market-neutral portfolio, with the intention of locking in that level of outperformance for the rest of the year. There would have been three problems with this. First, it is difficult to be accurately market-neutral. Second, it would have meant abandoning our principles (you might ask: “So what?”). Third, we would have had nothing to write about for the rest of the year.

Model Equity Portfolio for the week ending 22 May 2020

This week we intend to increase our notional positions in our favoured bank stocks, which continue to trade at well below their average historic valuation levels and some of which have gross dividend yields far in excess of T-bill yields. We will add Stanbic IBTC to our list of notional holdings of bank stocks. We will add two palm oil and rubber producers, Presco and Okomu Oil, to our list of national holdings, reasoning that their sales are related to international commodity prices and are therefore defensive during times of currency stress.

Nota bene: The Coronation Research Model Equity Portfolio is an expression of opinion about Nigerian equities and does not represent an actual portfolio of stocks (though market liquidity is respected and notional commissions are paid). It does not constitute advice to buy or sell securities. Its contents are confidential to Coronation Research up until publication. This note should be read as an integral part of the disclaimer that appears at the end of this publication.