In the banking system, liquidity is often referred to as the ability to fund increases in assets and meet the withdrawal of maturing liabilities at a reasonable cost. However, in this paper, we will dwell on the Central

Bank of Nigeria’s (CBN) liquidity management of the financial system. This is defined as a framework, set of instruments, and especially rules followed by the Central Bank in steering the amount of bank reserves in order to control their price (i.e. short-term interest rates) consistently with its ultimate goals (i.e., price stability), (Bindseil, April 2000).

The dynamics between the demand and supply of money is a crucial driver of interest rates. The mismatch in this relationship is carefully monitored by central banks worldwide and is a key factor in implementing monetary policy (Aoki, Benigno & Kiyotaki, 2018).

Tools for Systemic Liquidity Management

- Cash Reserve Requirements (CRR)

- Open Market Operations (OMO)

- Benchmark Interest Rate

- Standing Lending and Standing Deposit Facility

- Repo and Reverse Repo

Cash Reserve Requirements (CRR): This is the minimum amount of deposits commercial banks are required to hold with the Central Bank. As with all monetary policy tools, this rate will be determined based on the Central Bank’s monetary policy stance – expansionary or contractionary monetary policy.

Open Market Operations (OMO): This involves the buying and selling of money market securities by the Central Bank to control commercial and merchant bank reserves. OMO securities are sold when central banks seek to reduce the liquidity in the banking system and purchased to increase liquidity.

Benchmark Interest Rate: The Central Bank of Nigeria’s benchmark rate is the Monetary Policy Rate (MPR). This is the monetary policy anchor upon which all other interest rates in the economy is expected to revolve around. This is the rate at which the Central Bank is willing to lend to banks. The symmetric/asymmetric corridor is set around the MPR (the lower bound rate at which excess reserves are deposited with the Central Bank and the upper bound at which banks borrow from the Central Bank). The MPR and the corridor are designed to guide short term interbank rates around the MPR with the interaction of market players ensuring that money market rates revolve around these corridors.

Standing Lending and Standing Deposit Facility: The SLF and SDF provide commercial and merchant banks a window to access the Central Bank’s liquidity in time of liquidity shortage and provide an opportunity to invest excess liquidity overnight, thus facilitating and fostering an efficient payment system.

The setting of the SDF and SLF rate priorities interbank market liquidity over CBN facilities.

Repo and Reverse Repo: The CBN also provides the opportunity for Deposit Money Banks (DMBs) to present eligible assets as collateral to access funding from time to time to aid interbank trading, smooth functioning and efficient settlement of transactions with counterparties.

The Objectives of Financial Liquidity Management

- To foster Price Stability

- To facilitate productivity, output and economic growth

- To promote maximum employment.

It’s impossible to achieve all three policies at once; depending on the economic cycle, central banks usually prioritize two at any point.

The Dilemma of Liquidity Management in Nigeria: Price Stability vs Economic Growth

The CBN has historically been faced with the challenges of high inflation and economic recessions concurrently (Sobrun & Turner, 2015). Central banks battle low inflation in recessions and high inflation in periods of economic growth. The peculiarity of the Nigerian economic structure leaves the Apex Bank with the dilemma of choosing between two conflicting policy objectives.

The Central Bank of Nigeria has used its monetary policy tools to prioritize both price stability and economic growth. It has eased its monetary policy rate, provided lending guidelines to banks designed to increase lending, even as inflation continues to rise. This is a dilemma to liquidity management because measures to spur economic growth are inflationary, while the actions to tame inflation are contractionary. This raises the question of the best approach and combination of policy tools to be deployed to reach these objectives. To answer this question, is it important to understand the factors that have historically driven economic growth and are currently driving inflation in Nigeria.

GDP Growth and Interest Rates

In 2016, the CBN opted to raise its policy rate to combat inflationary pressure and support exchange rate stability despite the contraction in output. However, it eased the monetary policy rate to support growth while inflation and exchange rate pressure built up in 2020. Due to the peculiarities of the Nigerian economy, rising interest rates clearly is not a contractionary factor (as seen in the graph above). Given that the current inflationary environment is driven by non-domestic demand-related factors (Naira devaluation due to oil dependence of the economy and food supply shocks), higher interest rates may not necessarily pose a risk to economic recovery.

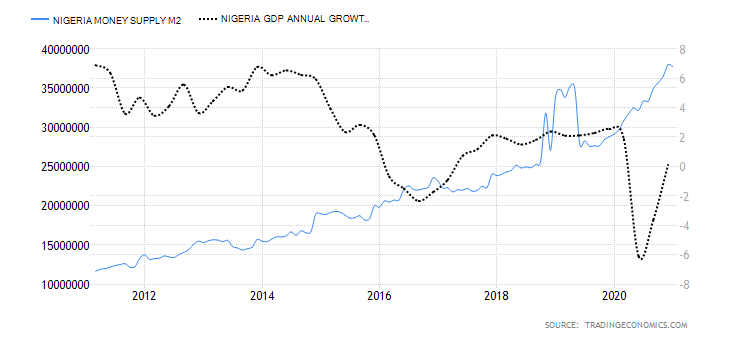

GDP Growth and Money Supply

There appears to be no direct correlation between money supply and output growth over the past ten years. Hence, increasing liquidity cannot be seen as a driver of economic growth.

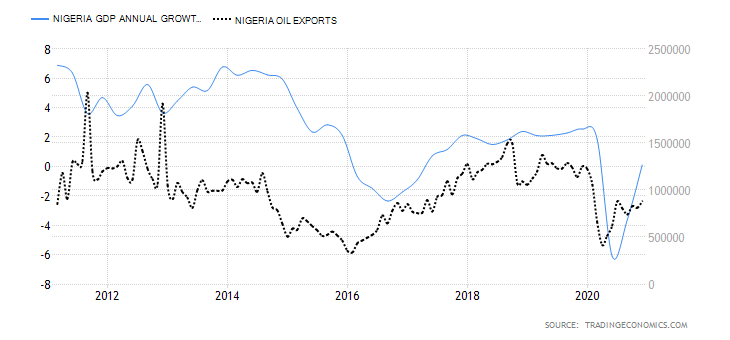

GDP Growth and Oil Exports

The graph above makes this point more straightforward. Economic growth in Nigeria is more correlated to external factors (supply/demand dynamics of the crude oil market) than domestic interest rates. In fact, monetary policy has taken a reactive stance to these external factors.

The Next Era of Liquidity Management in Nigeria: Inflation Targeting

The fiscal policy authority should focus on diversifying the economy in terms of boosting export earnings for increased FX receipt, increase direct spending in productive sectors, human capital development and incentivise the private sector to create jobs. They should also support MSMEs to thrive through investments in power and transport infrastructure.

Monetary policy authorities on the other hand would need to target rising inflation. Central Bank liquidity management over the years has not been without challenges. As advanced economies grapple with low inflation and low growth, Nigeria should continue to focus on boosting aggregate demand through targeted fiscal policy measures and taming inflation through monetary measures.

References

- Liquidity Management in Nigeria Deposit Money Banks: Issues, Challenges and Prognosis; Godwin E. Bassey

- https://www.cbn.gov.ng/Out/EduSeries/Liquidity%20Management%20by%20the%20CBN.pdf

- https://hbr.org/2016/12/mapping-frontier-economies

- IMF Working Paper; A Greater Set of Policy Options to Restore Stability

- https://www.imf.org/en/Publications/GFSR/Issues/2021/01/27/global-financial-stability-report-january-2021-update

- IMF Working Paper – Monetary Policy Transmission in Emerging Markets and Developing Economies

- Brooking Global Economy & Development – Monetary Policy Challenges for Emerging Market Economies by Gill Hammond, Ravi Kanbur, Eswar S. Prasad

- https://www2.deloitte.com/us/en/insights/economy/monetary-policy-emerging-economies.html

- BIS Working Papers No 508 Bond markets and monetary policy dilemmas for the emerging markets by Jhuvesh Sobrun and Philip Turner

- NBER Working Paper Series Monetary Policy in Emerging Market: A Survey Jeffrey A. Frankel

- Monetary and Financial Policies in Emerging Markets Kosuke Aoki, Gianluca Benigno and Nobuhiro Kiyotaki

- Monetary Sector Model for Nigeria, Research Department Central Bank of Nigeria

- Central Bank Economic Report, November 2020

- A synthesis for liquidity management in the central bank of Nigeria

- https://www.project-syndicate.org/commentary/emerging-markets-unconventional-monetary-policy-by-piroska-nagy-mohacsi-1-2020-08?barrier=accesspaylog

- Nigeria Inflation Rate | 1996-2021 Data | 2022-2023 Forecast | Calendar | Historical (tradingeconomics.com)

- The Role of Central Bank of Nigeria’s Analytical Balance Sheet and Monetary Survey in Monetary Policy Implementation by Sani. I Doguwa and Sunday. N Essien. CBN Journal of Applied Statistics Vol.4 No.1 (June 2013)